The False Start Market

Last year I thought we were going to have a recovered housing market in the spring. This year I thought the same thing was going to happen. Both times were dashed. I am starting to feel like Charlie Brown running up to kick the football only to have Lucy pull it away at the last second. Except in this version Lucy is a combination of tariffs, geopolitical chaos, and a bond market that just doesn't believe us anymore.

Let me explain what I mean by a false start, and then I'll get to the part that actually matters.

The Pattern

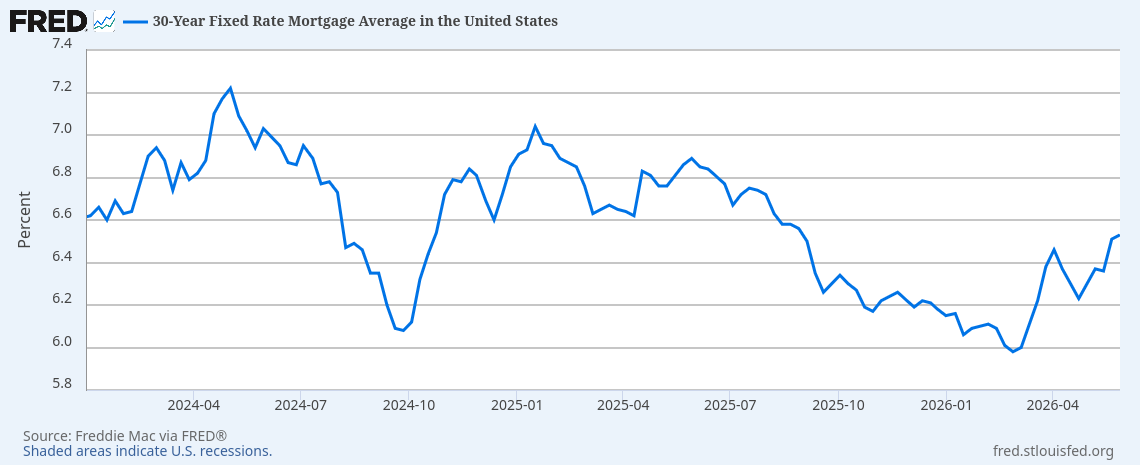

Spring 2025. Rates were starting to soften coming off 7% highs, inventory was absorbing a little better, buyers were getting off the sidelines. Then the tariff announcements hit like a freight train and the market went on ice. Nothing changed right away, but there was uncertainty and rates went right back to 7%, enough to postpone plans to buy and leaving sellers with the feeling of dread as their equity started to melt. The spring push that everyone was expecting just didn't materialize.

Fast forward to spring 2026. Same setup, different trigger. Mortgage rates even flirted below 6% in late February, then the Iran situation created the same freeze response. Oil shocks, equity market volatility, and uncertainty all came back. Buyers who were warming up went back to the couch. This is now twice in two years that we have seen the heating spring market and had something external shift it dramatically an interrupt the normal annual residential real estate cycle.

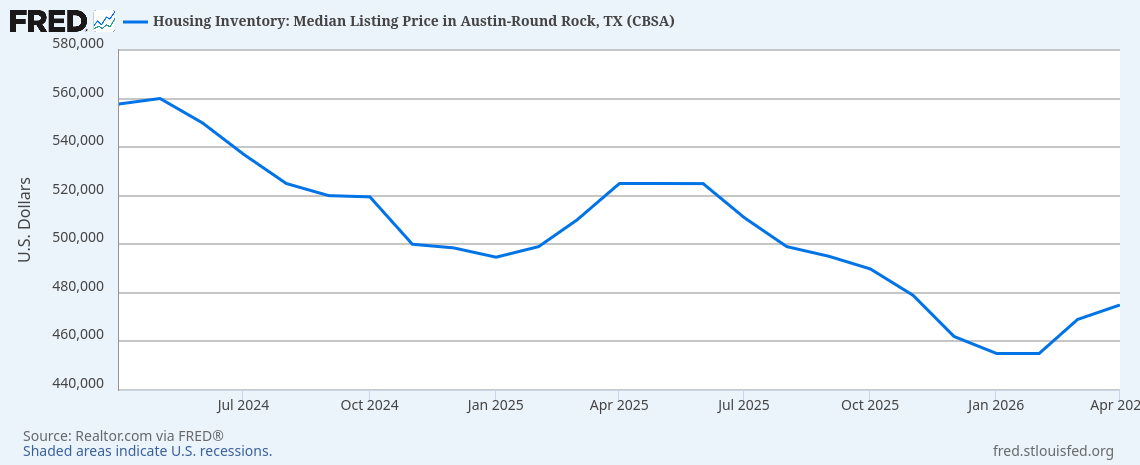

The headline data reflects this pretty clearly. New listings are down year over year, prices have continued to fall, and about half of all active listings have already taken at least one price cut. That is not a recovering market. That is one that is softening like butter.

The Rate Problem Isn't Going Away

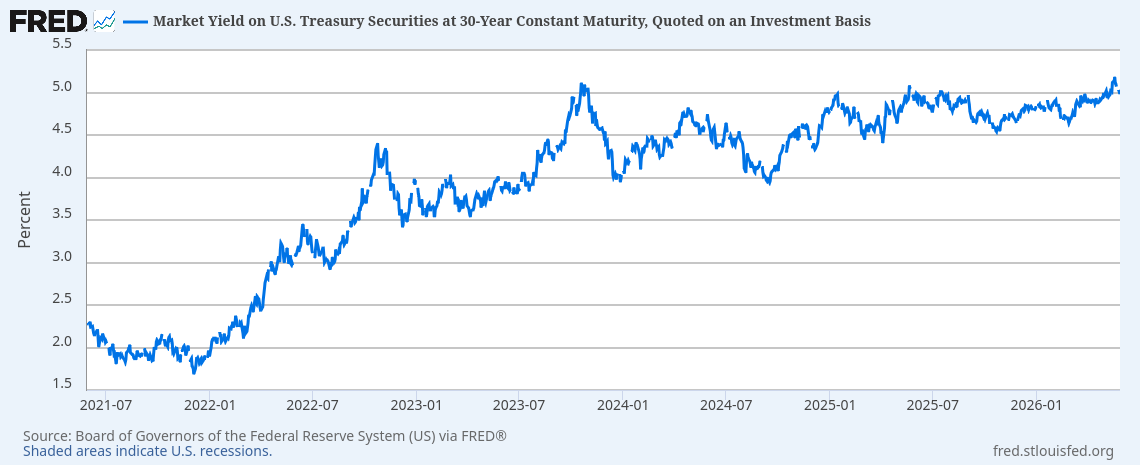

The 30 year treasury has pushed past 5%. That number matters because it reflects something important: investors aren't as enthusiastic about holding US debt as they used to be. There are a lot of reasons for this that I won't get into here, but the short version is that when the world starts parking money somewhere other than US treasuries, yields go up to attract buyers. While this doesn't directly move mortgage rates, it reflects investor sentiment and willingness to lend. This isn't a Fed problem you can solve by swapping out the chairman.

Speaking of which. The Fed is stuck. They know they need to be careful about cutting rates because inflation has been ticking back up, partly driven by oil shocks. Even a new Fed chair arrives at the same math. You can change the person doing the calculation but not the numbers going into it. I don't see meaningful rate relief coming this year. Ending the whatever you want to call the conflict in Iran would be a good start, but it will take some time to undo the damage and get supply chains back to normal. That normal is also going to be different than before, we just don't know what it will look like.

What Sellers Are Doing Instead

Sales prices are going down which is the market's way of telling you demand is soft. But here's the wrinkle. A lot of sellers who can't get the price they want are choosing to lease their property instead. This makes sense emotionally and many of those would be sellers have some cheap loans too. Rather than take a hit on the sale, they become accidental landlords and put their home into the rental pool.

The downstream effect of that decision is that we now have a lot more rental supply than we did a few years ago, which is driving rent prices down. So if you're a renter right now Austin is actually a pretty good place to be. If you're a buyer hoping that tighter inventory will push prices back up, this behavior is working against you because sellers are choosing to remove their home from the for-sale market rather than meet the market where it is.

Georgetown is the notable exception and I find it genuinely interesting. Premium out-of-state relocators and local move-up buyers with equity are going there and they are not price sensitive in the same way. That market is telling a different story and it's worth watching. It may be an older demographic that is less sensitive to a job or rates. This is pure speculation though.

The AI Layoff Overhang

Austin's job market has held up better than most cities nationally, but tech sector anxiety is real and it is keeping some buyers on the sidelines. AI-driven layoffs and the fear of them are not the same thing economically but they produce the same behavior: you don't buy a house when you are not sure if your job exists in eighteen months. That uncertainty is in the air right now and it is a meaningful drag on the buyer pool.

The Exception

AMD and DELL have had explosive stock performance recently. Both are up over 250% in just the last 6 months! If you hold a meaningful position in either of those, your net worth just went up materially on paper. That is what wannabe economists like myself call a wealth effect, and historically it does push some people into large purchases including real estate.

I say on paper because that is the key phrase. We do not yet know if these gains stick. Tech stock runups have a history of being irrationally exuberant and then heart breaking. The people who went out and bought a house at the top of their comfort level before the correction tend to regret it. I think most of those holders know this, which is why I don't believe that cohort has hit the Austin real estate market yet in any meaningful way.

But here is the thing. If even a fraction of those holders decide to lock in some of those gains and deploy them into real estate, that will create real buying pressure in a specific price bracket. I don't think it has happened yet. When it does you will see it in the data before you feel it on the ground. Watch the contract-to-price-change ratio in the $600K-$900K range. If that starts compressing, that's our signal.

The Case for Buying Right Now Is Actually Pretty Good, For the Right Person

Sellers outnumber buyers. Prices are still declining. Half the listings you see have already cut their price at least once. The geopolitical triggers that froze the market earlier this year have not resolved but they have been priced in to some degree. Sellers who have been sitting on their home for six months are negotiating. Terms matter right now as much as price. Concessions, rate buydowns, closing cost contributions — these are all available in a way they were not during the 2021 and 2022 madness.

I don't know if the market has hit a bottom. I want to be clear about that. There are too many downward forces at play — rates staying high, job uncertainty, continued soft demand — for me to plant a flag and say we are there. But if you are a buyer with a strong equity position looking to take a relatively modest loan, your hand is strong. You are not competing against a lot of people like you. The market is pricing for the median buyer and you are not that.

The risk is that prices fall further after you buy. That is real and I won't pretend otherwise. The offset is that you locked in favorable terms in a buyer's market, your loan balance is small relative to the asset, and if rates do eventually fall you refinance into something better.

The perfect thesis here is simple: higher equity, lower debt, favorable terms, and patience. If your stock gains made that possible, now might be the time to let real estate do the thing it has always eventually done.

We will see how this one ages.

As always, question everything and don't take suggestions as absolutes. These are written from a perspective of our experience and offering our insight, however limited. We're not perfect and get things wrong... but not on purpose.