Is SVB a One-off or Is There Worse to Come?

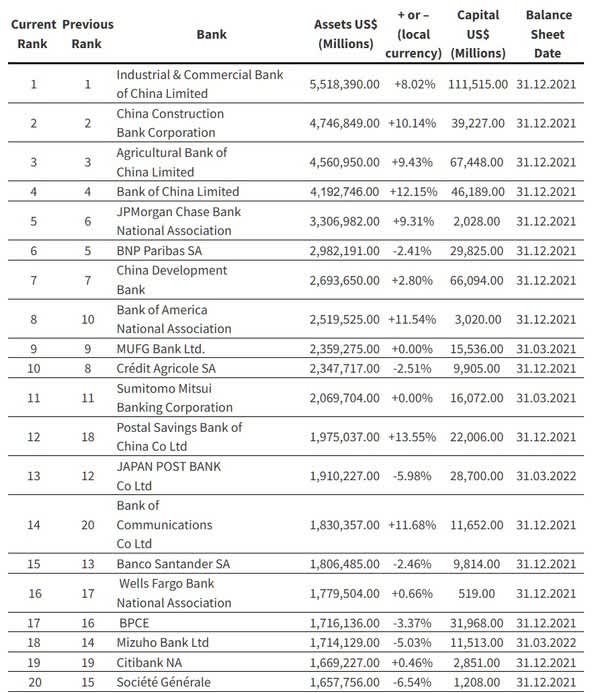

Here Are the Top 20 Global Banks (By Size)

This list is according to LexusNexus as of January 30th, 2023, you can click the chart above to go to the full list, SVB was not in the top 50.

The largest US bank is JPMorgan Chase, however, it is very interesting to note the amount of capital each bank keeps compared to its assets. US banks hold a lot less compared to the large Chinese banks, although you have to assume their reporting is also honest. You can see some of the other leading US banks in the list as well, all of which are highly leveraged. Keep in mind this list does not underwrite small regional banks which may be even more stable but are too small to be evaluated.

Here are some darts for you to throw at your next cocktail party:

- The Fed did it - SVB fundamentally failed due to interest rate risk, something that hasn't been around for many decades, and the very fast pace of the Fed raising rates caught them off guard and caused a gap they couldn't cover. So you could point your finger at the Fed, but that information has been well known, so it's a matter of how fast can you expect a bank of this size to turn the ship when rates go up at this clip.

- Insider Lobbying - SVB (and many others, so it's not just them) lobbied DC to raise the limit for certain financial stress tests and audits from $50B to $250B. This bill passed 258-159 (so not one sided) This left fewer than 10 big US banks subject to these type of stress tests, although to be fair the vast majority of banked cash is in those banks.

- It all comes down to leverage - lowering reserve requirements and limiting stress testing mean a financial institution has the ability to risk more and earn more as long as things go according to plan. Slow growth is boring, so bored bankers want to leverage more, at least the ones at SVB. They're certainly not alone. It's the oldest story in the book. Whether you are a bank, a home owner, or an investor, you can optimize for longevity (lower leverage) or high return (lower survivability).

As I have aged, I have moved more toward the latter. I still get to play the game, and attempt to keep my ego out of maximizing returns (and risk). Instead, I just want to grow safely and watch the train wrecks go by from my solid and boring low-leverage balance sheet.

So far we just have one bank failure due to mishandled interest rate risk (lots of 10 year bond at 1.25% while paying 5% in today environment) and poor management (no risk officer for the last 8 months). Share holders and bond holders in SVB are going to get crushed but small depositors should retain their funds due to FDIC insurance. There doesn't seem to be much contamination to other banks that we can see yet. It's still early, and this bank was still small compared to the top 10, total assets under management were around $220B. Chase by comparison is $2.6 Trillion, over 10X larger. Grant Cardone would be proud.

So What Does This Mean for Real Estate?

In the short run, bank stocks have been crushed by the uncertainty and rates have actually gone down a little mostly out of anticipation of a Fed slowdown. Now the real question becomes what does the Fed actually do? They have been aggressively hiking rates to cool inflation and slow the economy. Well ok Fed you did it, and at least contributed to the collapse of a $220B bank. So do you keep hiking rates, take a pause, or even pull back?

This could be a tipping point where the Fed re-thinks its rate policy and maybe slows down earlier than they originally expected. They're damned no matter what they do. Raise rates, make the economy worse and kick over more banks, lower rates, inflation runs hot and we all start buying wheel-barrels. So which devil is worse? If you believe Powell's earlier rhetoric of not stopping until inflation is below 3%, then they will do at least a small hike. Wall street thinks the Fed will slow or even pause the rate hikes after this event. You can tell because real estate stocks are all up on anticipating a pause, but this narrative benefits them so they are certainly seeing through rose colored glasses. Regardless of what happens, it's going to be interesting. Oh that's also a terrible finance pun.

Some people are into the Kardashians, I like finance policy drama.

Dates to watch:

- Next Fed meeting - Wednesday , March 23, 2023

- USBLS Inflation Data - April 12th, 2023

As always, question everything, don't take suggestions as absolutes. These are written from a perspective of our experience and offering help. We're not perfect and get things wrong, but not on purpose.

My son Elliot turned 10 last week on the Ides of March. Mr. Man is now in the double digits and is a hard core Zelda fan.