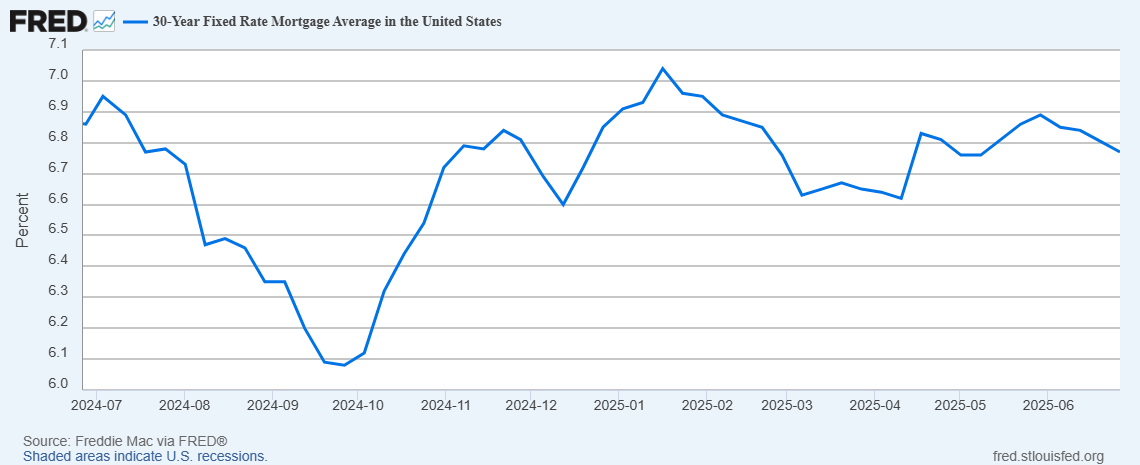

Interest rates have been pretty much flat for the past six months with the exception of last October when they dipped into the low 6.0% territory.

Normally I would say this is a good thing. It makes the world predictable. As a buyer you know how much money is going to cost and you don't feel especially bad or good anticipating the rates will go up or down in the future. This gives you one less thing to worry about and makes the equation for deciding what to do easier.

However, markets and politicians love lower rates for all of the obvious reasons. Cheaper debt allows governments to refinance at lower rates which is a very pressing problem for the US Treasury right now. It allows more buyers to afford stuff. So it stimulates the economy which grows jobs, spending, economic output, the number of replies you get on tinder, your ability to get a pony, and more votes in the midterms. And it all lasts until inflation shows up to ruin the party. It's a short term fix, but one that policy makers can't help themselves but use when they can.

Short Term Outlook

The current administration is desperate to get a win, even if it is short sighted. While the president can't dictate what the Fed does, this one is trying his best to do just that. While Powell's term ends in May of 2026, if there is any angle in which Trump can get him out sooner he will. His candidates are all firm yes-men, and while the Fed is supposed to remain impartial, his picks will certainly bend the knee and do as he asks. The one caveat to this is that Fed decisions are made by a board of seven, but there is also political pressure inside the Fed to line up. We have one year for Powell to hold out and keep inflation at bay. So if you are Trump and you can't get rid of Powell for a year what do you do?

Well as a concession without outright lowering the FED funds rate, since 2008 the FED has increased the amount of money banks are required to hold at the FED in reserve. This is ostensibly to create a cushion to prevent events like 2008 from happening. Well it's been a while so maybe it's time to relax that requirement and see if history repeats itself. The current FED balance sheet shows about 3.4T (Trillion) in deposits held by depositing institutions. A new proposal would allow those amounts to drop in proportion to the size of that bank compared to the total market share. This doesn't mean all 3.4T will come out at once, but it could become a much smaller number. This was only a few hundred billion before 2008 to give you some context.

So why does this matter? Well banks would reclaim those deposits and then be forced to put that money to work somewhere. The hope (the government's at least) would be that the liquidity from decreasing the reserve requirements would end up at least partially in US Treasuries driving up the demand and thus lowering interest rates which in term leads to all of the fun above. I'm going to need a new pony brush.

This might move the needle a little, until the heavy hitting Fed yes man can get into position. So in the next 12 months we may see some pressure to lower interest rates with these tactics. By next May we could see a politically motivated free fall.

Long Term Outlook

The long term debt cycle has certainly bottomed out back in 2022 when rates were effectively 0% for a short time. So it seems pretty clear that we are going to be on the up stroke of that cycle for some time. We just don't know what the next peak will look like. There will be peaks and valleys along the way, but usually they end with a high rate environment meant to cool inflation which is very painful and an economic contraction. This is just my reading of the tea leaves for the long term.

1) The big beautiful bill will pass which will weaken the dollar because you can't lower taxes and increase spending without that happening.

2) Next year the FED chairman will be a yes-man and lower interest rates which will send everything soaring making borrowers and asset holders temporarily happy.

3) The US will use this window to refinance as much of its debt as possible.

4) Inflation will come roaring back in 2027.

5) The economy will not be strong enough to hold up to the pressure and the US will experience a recession, then inflation, then high interest rates (10%+) in order to tame our final free money party. This will likely send the incumbent political party packing.

What does this mean for housing?

Prices in Austin at least are down 22% off their peak in 2022, but still up 20% from 2019. I expect interest rates to fall slowly in 2026 then fast with a new FED chairman. At first this will soak up inventory in the market and stop housing prices from falling. Then prices will go up due to the free money party. At that point you have two pretty good options.

1) Buy before Powell is replaced

2) Refi your existing properties with super low debt at overall prices when you bought them

3) Sell when rates are 1%

Once the high interest rates kick in, prices will plumet and a lot of buyers will end up under water and we will have a repeat of 2022. You will be sitting pretty if you either sold or locked in low rates with older smaller loan balances. Just like today, landlords that are cash flowing and profitable are the ones that bought their assets a few years ago, kept them and refinanced the debt when rates were low. We will see a bigger version of that same story in 2027 to 2028.

The best time to buy is before rates go down but inventory hasn't been fully absorbed. There is no way to know what that exact date will be, but likely before May 2026 when Powell’s term ends.

It's going to be very interesting to re-read this article in 2028. This is speculation, not financial advice.

As always, question everything and don't take suggestions as absolutes. These are written from a perspective of our experience and offering our insight, however limited. We're not perfect and get things wrong... but not on purpose.