Houses, Not Just for Investing

Last month we held our first in a series of house concerts for our friends and clients here in Austin. Wendy Calonna was our inaugural local performer and despite the rain, we all had a great time listening to some local music in person, like people not suffering from a plague. Our next one will be in January and will feature Kalu James. You have probably already received an invite. If not, email me. Maybe we'll get lucky and it will be dry then.

The Cpi - What is it Good for?

The CPI numbers came out this week and inflation is at 7%, lower than the last two months (8% and 9% respectively), but still positive. So the boat is still sinking, but slower. The markets reacted with a big rally and a drop in mortgage rates. On Tuesday they touched just below 6%. Over the following two days the hangover showed up and the market lost all of those gains and then some.

As of Thursday afternoon we're down for the week, which is what I would have expected. It's literally like the market is drunk and can't find its way home. So despite the early optimism of a soft landing it looks like the Fed is still keeping the pedal down and more rate hikes are coming albeit slower than 0.75% per meeting we've seen in previous months.

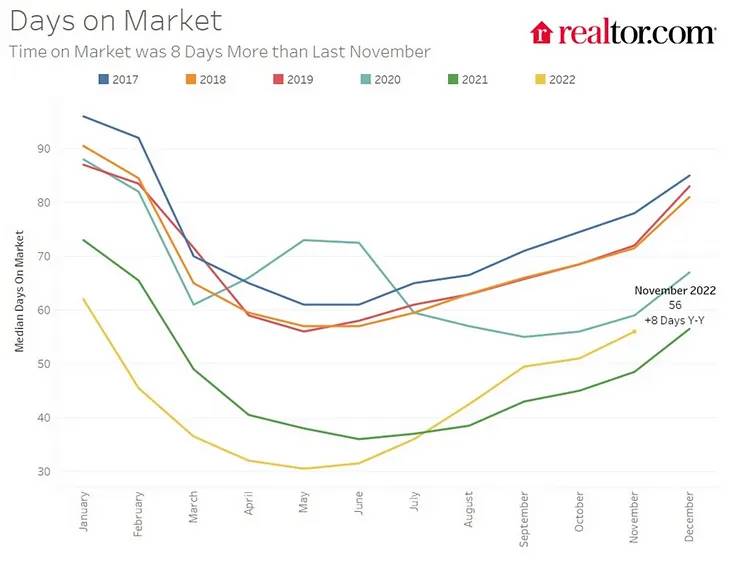

So what does this mean for housing? Well national inventory levels are at 56 days according to Realtor.com, an eternity by 2021 standards, but still lower than 2017, 2018, and 2019 when no one was panicking although both prices and rates were lower then.

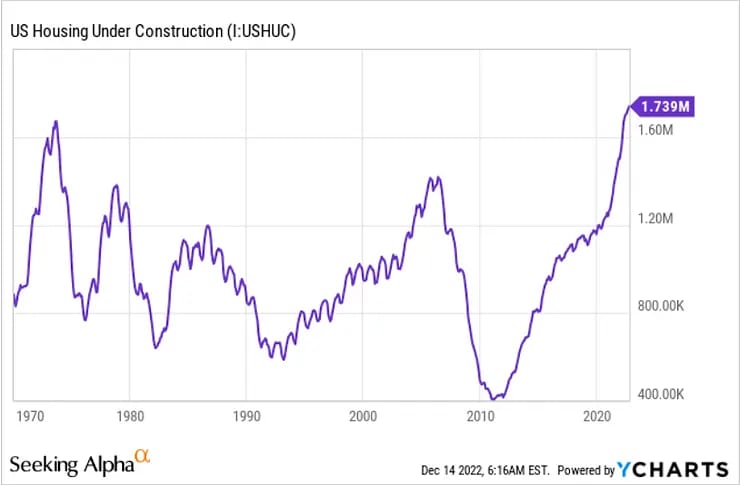

So in a long term view we are still tight on housing, more so than even the pre-pandemic years. However it's also worth noting that housing starts are also at an all time high from everything that was started in the boom of 2021, so that inventory will start to show up in 2023 for sure. (Keep in mind the chart below is a national meta value and there is a deficit of new builds that we are making up for - the area under the curve is more important than a local maxima)

Seeking Alpha

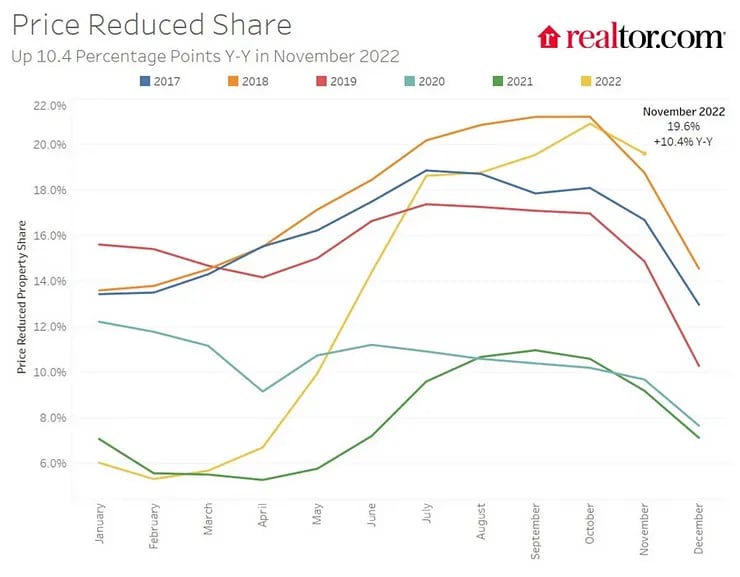

So the good news for buyers is that prices are being discounted more so than any time in the past 5 years and increasing inventory will likely put further downward pressure on housing prices in 2023 assuming buyers are still shy. 2018 was actually 'worse' in terms of discounting except for November where this year makes a new high. Really we are returning to a housing market that we had before the pandemic, and that shift started in the middle of 2022. So the sky is not yet falling despite the headlines you see out there. Nothing is single variable though, and more buyers will have to move in the spring, so it's a matter of which force is greater which we can't know for sure, but it is fun to read the economic tea leaves.

Right now we have rates right around 6% which was a ho-hum rate between 2003 and 2008 although prices are higher now so the median mortgage payment has increased rapidly in the past year. This is also a result of inflation, but this is something the Fed wants to lower, it's better for the market to be lower and is also likely to fall to bring the market back into balance and people simply can't afford these kind of payments without much cheaper money.

The market will certainly react to this. If it falls, it will be a combination of lower prices in the short term and perhaps even lower rates in the long term. Even with the CPI continuing to decrease 1 point per month, it will take another 4 months to get below 3%. Assuming that happens we could see some rate relief then but it won't be sub 4%, the Fed will be slow to reduce rates until inflation is 'fixed.' A good portion of the CPI is also housing, so housing costs will have to come down to get the overall CPI in line.

Now once spring shows up, more buyer demand will return and we may see a curve similar to 2017 or 2018. It's a matter of how much buying pressure there will be to offset higher rates and inventory. We shall see... I'm sorry a more normal market is not as exciting as a collapse. Keep this in mind as well, even in the worst of the 2008 market crash, Austin only dropped 15-20%. If that happened we would still be ahead of 2020. The short term is super fun to speculate and panic about, but the long term is pretty consistent.